This article was first published on 1 July 2016 by Su-Lin Tan in www.afr.com picture by Jessica Hromas

Sydney and Melbourne housing prices continue to defy a cooling, posting another price rise in the month of June, according to Corelogic’s June Home Value Index.

While foreign buyers were once thought to be mainly responsible for the the rise in house prices in the last three years, local homebuyers and investors showed their buying power buoyed by record low interest rates. The major banks have all ceased foreign lending.

“The impact of interest rate cuts from May is working its way into the system now,” Corelogic senior research analyst Cameron Kusher said.

“It’s not exclusively foreign buyers but local buyers…who have seen their home prices increase by half, so the wealth effect is high.”

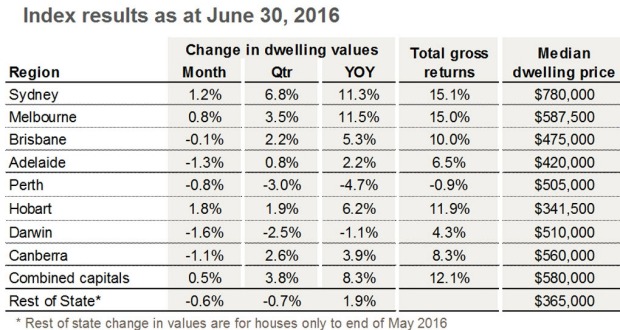

Index results 20 June CoreLogic

Sydney house prices have risen another 1.2 per cent in June, but lower against the May rise of 3.1 per cent.

Melbourne rose 0.8 per cent versus 1.6 per cent last month.

Hobart also continues to show strong capital growth scoring a 1.8 per cent rise in housing prices in June.

But the rest of the other capital cities recorded a fall in housing prices; as a result, capital city dwelling values barely rose at an overall 0.5 per cent in June.

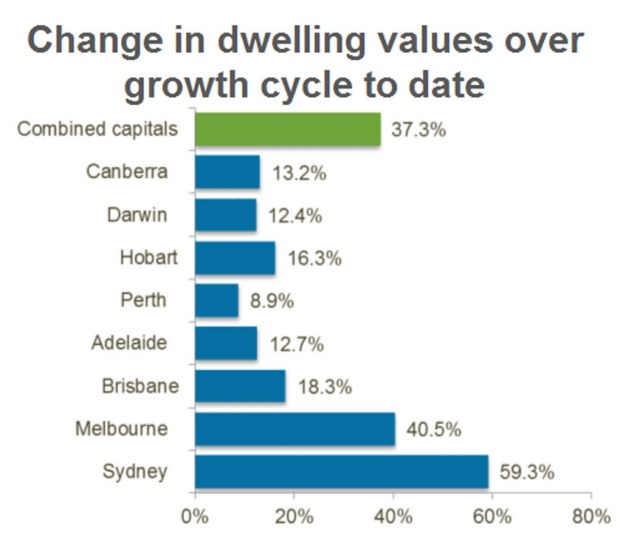

Change in dwelling values over the growth cycle to date CoreLogic

For the first half of the year, capital city dwelling values have moved 5.5 per cent with the most substantial capital gains located in Sydney at 8.9 per cent, Hobart, 8.5 per cent and and Melbourne at 5.8 per cent. These numbers were smaller than the same time last year.

“While the higher rates of capital gains in Sydney and Melbourne can be tied back to strong economic conditions, and high rates of population growth, the same cannot be said for Hobart where economic conditions and migration rates are gradually improving from a low base,” Mr Lawless said.

“The strength in the Hobart market comes after a long period of underperformance…potentially, the Hobart housing market is being fuelled by the sheer affordability of housing and a renewed trend towards Melbourne and Sydney buyers unlocking their equity to make lifestyle housing purchases.”

Gains starting to slow

While the rebound in the last few months watered down the cooling that started in the final quarter of 2015, Corelogic research director Tim Lawless said the those gains are starting to slow.

“The monthly growth rate reduction is likely to be very much welcomed by state and federal government policy makers and regulators who may be concerned about a sustained rebound in capital gains,” he said.

Mr Kusher also predicted there would be reprieve for Sydney and Melbourne in the second half of the year and spring, the traditional property buying season, could be a “fizzer”.

The uncertainty caused by the Brexit vote is likely to slow down price growth as is the slower turnover of stock in Sydney and Melbourne, Corelogic said.

“Some positive news for Sydney buyers is that there are early signs that Sydney’s housing market may be starting to turn in favour of the buyer,” Mr Lawless said.

“We’re seeing homes in the city taking longer to sell and vendors are starting to offer larger discounts on their asking prices in order to make a sale.”

“The typical Sydney home is now taking 40 days to sell compared with 26 days a year ago and discounting rates have risen from 5.5 per cent a year ago to 5.6 per cent.”

“In balance, Australia’s two largest cities are facing increased affordability challenges that are likely to negatively impact the trajectory of dwelling values and activity as more prospective buyers are blocked from the market.”

As a consequence of rising prices, gross rental yields continue to slip nationally, pushed mainly by the deterioration in Sydney and Melbourne.

The gross yield on a house is now averaging 3.2 per cent and units are averaging 4.1 per cent.