Despite the recent international stock market volatility, according to an investment report by Russell Investments, the average house in Melbourne returned an average of 49.8 % over a five year period until June 2011. This equates to an average annual return of 9.98 per cent per year, which is a hefty contrast compared to the stock market, bonds, or commodities. This performance has also continued well into 2012, 2013 and 2014, with reports reconfirming this trend in 2014.

What’s more astounding, is despite all the constant doom and gloom predictions, and in light of major international economic turmoil, the Australian Residential Property Market has managed to return an average of 10.1 per cent for the 10 year period until June 2011, and a staggering annual average of 11.6 per cent of a 25 year average until June 2011.

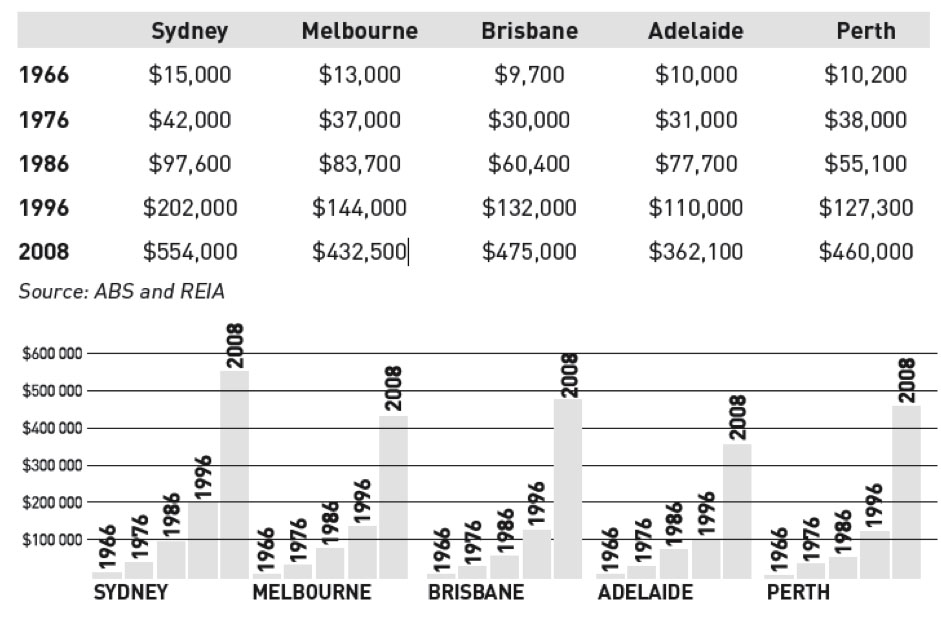

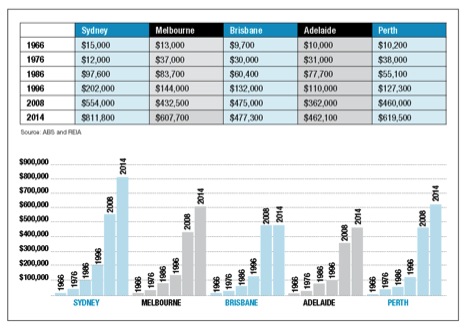

Current data from the Real Estate Institute of Australia (REIA), and the Australian Bureau of Statistics (ABS) indicate, in contrast to the volatility of the European and US markets, Australian residential property in all the major capital cities has demonstrated a level of resilience that has managed to defy the expectations of the “doom and gloomers” for over three decades. The table below depicts median price increases across the major capital cities in Australia since 1966.

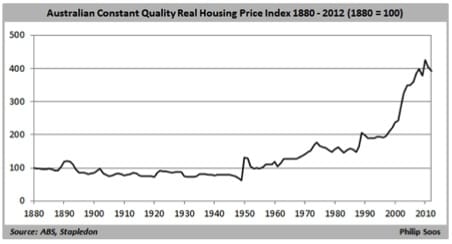

The above figures show an amazing track record experienced by the residential property market in Australia. This track record of consistent capital growth appreciation holds true for historical periods of time of well over 100 years, as can be seen from the table below.

Despite of all this, the constant fear-mongering bandwagon, which the media loves to jump on, has created a very nervous overall consumer sentiment in Australia towards the future of the Residential property market, and the notion that is will simply end up crashing…sometime in the near future, so let’s examine the track record of the media and the ‘doomers and gloomers’ over the last 50 years;

The extreme Armageddon-like Australian property outlook portrayed by the likes of Harry Dent, Dr Steven Keen and Jordan Wirsz have been extensively publicised recently by the media in 2008 to 2014, spreading wide concern amongst first home buyers, and the largely uninformed mum and dad home owners.

Whilst these views are not only unfounded, flawed and often sensationalised, they also have a tendency of robbing the average Australian of the opportunity to invest into an asset class that has proven its resilience to global economic downturns and recessions for well over 100 years, essentially scaring them from buying an investment property.

On this note, the most extreme point of view was voiced by US real estate analyst, Jordan Wirsz, who believes that Australia is heading towards a “property bloodbath” as the global economic downturn spreads, with a decline in property prices of 60 per cent. Mr Wirsz was quoted saying:

“Right now is not a time to be buying real estate in Australia,”

and further to this, he stated;

“The market has slowed substantially but residential prices are likely to fall up to 60 per cent, possibly even more, within five years.”

Similar doom and gloom opinions were voiced by visiting US economist Harry Dent who recently said Australian house prices were 50 per cent overvalued, and were destined to crash, just like they did in the US.

Conversely, these extreme views have been largely slammed by Australian property experts, leading economists, and property research based companies including, but not limited to, Residex, RP Data, AMP, ANZ, HIA, BIS Shrapnel, HSBC leading economist -Paul Botham, and the list goes on. To put this statement into context, a 60 per cent decline in property prices across Australia would translate to median house prices in Sydney dropping from $660,000 to $264,000, Melbourne dropping from $550,000 to $220,000, and Brisbane dropping from $580,000 to $232,000. It’s laughable, isn’t it?

Did I mention that this proposed ‘market crash’ is supposed to take place in an Australian economic environment which includes low unemployment rates, historically low interest rates, a strong Australian dollar riding on the back of a resource and commodities boom industry, Foreign Buyers & SMSF investment?, not to mention a massive surge in incoming migration, most of whom will settle in the major capital cities, with a back drop of a decline in housing construction and shortage of dwellings of approximately 160,000 by 2021?

Before we examine the basis on which most of these doom and gloom arguments rely, keep in mind that this is certainly not the first time in the last 50 years that predictions of the Australian Property Market crashing have been made by so called experts, and academics. In all instances they were proven wrong, as the Australian Housing Median Prices continue to defiantly appreciate decade by decade. The table below depicts median price increases across the major capital cities in Australia since 1966.

Here is a short list of major economic events, both local and global that triggered a flurry of media articles and predictions that the Australian Property market would crash;

- Early to mid 60’s Australia was experiencing a major credit squeeze and finance dried up. Banks lending policies were tightened, resulting in an environment where it was very difficult to borrow any money to buy property. Due to the inability for most Australians to enter the property market, Academics and ‘Experts’ predicted that the Australian property market would crash. They were wrong.

- The late 60’s Poseidon bubble, saw the price of Australian mining shares soar, especially in the late 1969, then subsequently crash in early 1970. This ‘stock market bubble’ was triggered by the Poseidon NL company’s discovery of a promising site for nickel mining in September 1969. As a result, academics and ‘experts’ predicted that the Australian property market would crash. They were wrong.

- In the 70’s, Australia, along with most of the industrialized countries, except Japan, experienced an economic recession due to an oil crisis caused by oil embargoes by the Organization of Arab Petroleum Exporting Countries. The crisis saw the first instance of stagflation. Coined ‘the OPEC Oil Crisis’, this global event created a media frenzy of ‘Doom and Gloom’, and academics and ‘experts’ again predicted that the Australian property market would crash. They were wrong.

- The early 80’s saw ‘a severe global economic recession’, affecting much of the developed world in the late 70’s and early 80’s. The United States and Japan exited the recession relatively early, but high unemployment would continue to affect other OECD nations including Australia through to at least 1985. Long term effects of the recession contributed to the Latin American Debt Crisis, the Savings and Loan Crisis in the United States, and a general adoption of neo-liberal economic policies throughout the 1980’s and 1990’s. Academics and experts again predicted that the Australian property market would crash in the mid 1980’s. They were wrong.

- After the Australian Property market refused to crash in the early to mid-1980’s, many Financial and Economic commentators got onto the doom and gloom band wagon, fuelled by the media, stating that Australian house prices were way overpriced compared to other industrialised countries, and that the property bubble would ultimately burst, leaving behind devastation. The prevailing argument here was that the average household debt had reached a ‘peak’ level, and based on academic deduction of the data, conclusions were drawn that people would simply not be in a position to borrow more money, and hence property would stagnate and eventually crash. At the time, property median prices in Melbourne and Sydney were about $85,000! They were wrong.

- On the 20th of September 1985 the Australian Government introduced Capital Gains Tax. The implications for Property investors were that any capital profits made from a sale of an investment property was now subject to a marginal tax rate of the investor. Financial commentators, financial planners, and so called experts predicted that this was going to BE THE END of property investing as we knew it. They were wrong.

- In 1987 we had the Stock market crash and what many referred to as a ‘1930’s type depression, with consumer sentiment at record low levels, the media once again jumped on the ‘doom and gloom’ bandwagon. With super funds being wiped out virtually overnight, many financial commentators and academics predicted that this prolonged period of economic uncertainty would be followed by a Property market Crash. They were wrong.

- In 1989 to 1991 Australia experienced historically record high interest rates and inflation. The early 90’s were the beginning of another recession; many of us will remember it for the famous quote from the treasurer, Paul Keating, “this was the recession we had to have”. Of the 18 OECD countries of reasonable size and development, 17 experienced a recession in the early 1990’s — a similar situation to the mid-70’s and early 80’s global recessions. The cash rate reached a staggering 18 per cent in the second half of 1989, and mortgage rates of 17 per cent, and many loans to businesses were well in excess of 20 %. Unemployment ended up peaking at 11.3 per cent, and once again many academics and experts predicted that the property market would crash. They were wrong.

- The Asian Currency Crisis, which gripped many of the Asian countries in mid-1997, raised fears of a worldwide economic recession. The crisis started in Thailand, and soon spread to neighbouring countries, eventually reaching as far as China and Japan, which directly impacted US and Europe. With major impacts on the various stock markets and managed funds around the world, many academics and experts predicted that the Australian Property Market would crash. They were wrong.

- The coordinated terrorist attacks on USA that took place on September 11, 2001, resulting in the collapse of the Twin Towers of the World Trade Centre created a virtual stock market freefall in the US and considerable drops were witnessed around the world. The uncertainty of follow-up terrorist attacks, created a downward spiral of negative consumer sentiment, and once again, academics and experts predicted that the Australian Property Market would crash. They Were wrong.

- The Sub-Prime Crisis in the US in 2006 to 2007 was triggered by a rise in sub-prime mortgage delinquencies and foreclosures, and the eventual collapse of subprime mortgage backed securities. Being essentially blamed on poor banking credit standards, greed, and speculation of assets continuously rising in value, the impact of this crisis triggered a plethora of media articles, and commentary of warnings that what happened in the US would eventually happen in Australia. In fact, many so called academics and experts went on record to say that the Australian household debts in relation to house prices were unsustainable, and the bubble would burst somewhere in 2009 to 2010. It didn’t. And as the table below depicts, the market slowdown was minimal, and was absorbed by the ‘buyers’ market almost instantly.

Bottom line, the ‘so called’ experts were wrong….again

- In 2010 to 2011, after defying the predictions of many academics and experts, the Australian Property Market once again continued to climb, with Melbourne hitting a new peak median price of $601K in December of 2010. This defiance to conform to predictions of collapse, lead to, in 2011 and early 2012, another campaign of predictions that the ever mounting household debt locked in the Australian housing market would ultimately lead to a ‘bubble bursting’ – with many families and household owners losing their life savings when the housing market corrects by 30 to 60 per cent of its current levels.

Perhaps the most memorable example of a doom and gloom article is that of commercial property advocate, Chris Lang, who proclaimed that Baby Boomers who do not sell their homes in 2012 will have to wait until 2025 before they could sell them, as no one would be interested in a large 4 bedroom houses in Melbourne and Sydney…

“Baby Boomers are facing an enormous challenge. And the sad fact is that they are probably not even aware of the problem. You see, if they haven’t sold their traditional inner-suburban homes before 2012 they need to be prepared to hold onto them until 2025, because there simply won’t be a market for that type of property before then.”

There is, in fact, an exhaustive list of other arguments that all predict that the Australian Property Market has to crash, ranging from demographic reasons, to economic reasons, stock market related reasons, to monetary and fiscal changes in Europe.